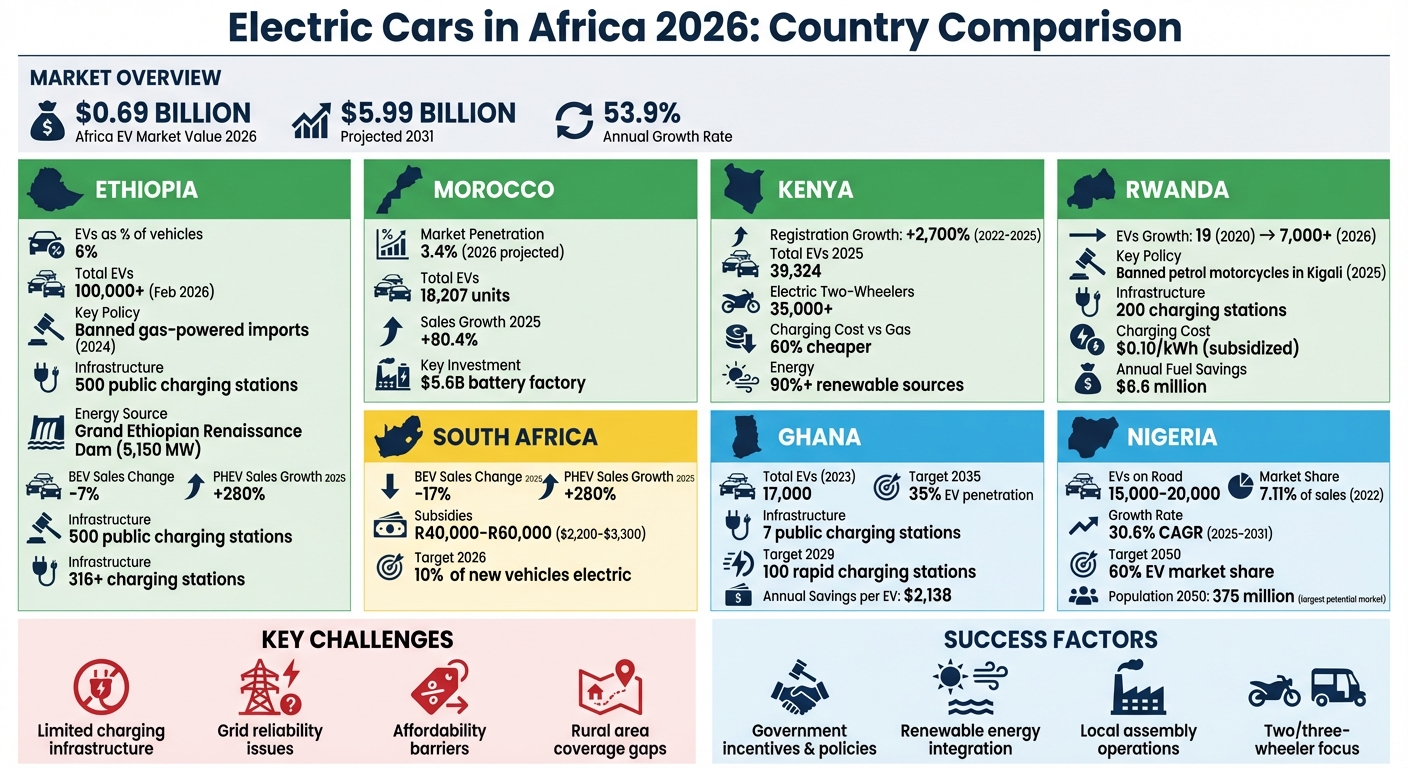

Africa’s electric vehicle (EV) market is growing fast, valued at $0.69 billion in 2026 and projected to reach $5.99 billion by 2031 with a 53.9% annual growth rate. However, progress varies widely across countries. Here’s a snapshot:

- Ethiopia: Banned gas-powered private vehicle imports in 2024; EVs now make up 6% of vehicles. Policies favor local assembly, and the Grand Ethiopian Renaissance Dam boosts clean energy supply.

- Morocco: A leader in EV manufacturing, with a $5.6 billion battery factory opening in 2026. EV sales climbed 80.4% in 2025, and Tesla has entered the market.

- South Africa: BEV sales fell 17% in 2025, but PHEVs grew 280%. Subsidies and solar-powered charging stations aim to address infrastructure and energy challenges.

- Ghana: Early-stage growth with 17,000 EVs by 2023. Limited charging stations hinder intercity travel, but government policies aim for 35% EV penetration by 2035.

- Nigeria: Fuel subsidy removal drives EV interest. Policies promote local assembly, but infrastructure gaps and unreliable electricity remain obstacles.

- Kenya: EV registrations surged 2,700% from 2022 to 2025. Electric two-wheelers dominate, supported by tax breaks and renewable energy.

- Rwanda: Banned new gas motorcycle registrations in Kigali. EV-friendly policies and battery-swapping networks are helping adoption.

Key challenges include limited charging infrastructure, grid reliability, and affordability. Most countries focus on two- and three-wheelers due to lower costs and practical use. Government policies, renewable energy, and local assembly are shaping Africa’s EV future.

Electric Vehicle Adoption Across 7 African Countries in 2026

1. South Africa

EV Adoption Rates

In 2025, South Africa’s electric vehicle (EV) market showed a mix of growth and setbacks. Battery Electric Vehicle (BEV) sales dropped by 17%, slipping from 1,231 units in 2024 to 1,018 units in 2025. This decline came despite the broader automotive market expanding by 15.7% year-over-year, with BEVs making up just 0.17% of the 596,818 vehicles sold.

On the other hand, Plug-in Hybrid Electric Vehicle (PHEV) sales soared, jumping 280% from 738 units to 2,808 units. This surge reflects consumer interest in vehicles that combine a 50-mile electric range with a nearly 500-mile total range, addressing concerns about BEV costs and range limitations.

Government Policies

To address these contrasting trends, the South African government rolled out targeted measures under the South Africa EV Policy 2025. For first-time EV buyers, direct subsidies range from R40,000 to R60,000 (around $2,200–$3,300). Fleet owners can access larger subsidies of R80,000 to R100,000 (approximately $4,400–$5,500).

The government has also set ambitious goals: by 2026, at least 10% of new vehicles produced must be electric, with this figure rising to 30% of all vehicles sold by 2030. Tax incentives are being offered to manufacturers to encourage local battery assembly and EV production. The ultimate goal is to establish a fully integrated EV manufacturing supply chain by 2035.

Infrastructure Development

While charging infrastructure is growing, it remains heavily concentrated in urban areas, leaving rural regions underserved. This issue is further complicated by South Africa’s unstable electricity grid and frequent load shedding, which disrupt traditional grid-connected chargers.

In response, CHARGE launched South Africa’s first off-grid, solar-powered EV charging station in Wolmaransstad, North West, in March 2025. This station marks the beginning of a planned network of 120 solar-powered chargers along major highways.

"Without a stable electricity supply, traditional grid-connected EV chargers could face disruptions, limiting their effectiveness." – VUKA Group

sbb-itb-99e19e3

2. Morocco

EV Adoption Rates

Morocco is stepping into the spotlight as Africa’s leader in electric mobility, showing impressive growth in EV adoption. Passenger EV penetration jumped from 0.7% in 2023 to 1.9% in 2024. By 2025, sales soared by 80.4%, reaching 5,311 units and claiming 2.6% of the market. Projections for 2026 suggest another leap, with sales climbing 36.3% to 7,237 units, pushing market penetration to 3.4%.

The growth trajectory differs across vehicle types. In 2026, plug-in hybrid (PHEV) sales are expected to rise 46.8%, outpacing the 30.1% growth forecasted for battery electric vehicles (BEVs). Dacia led the BEV market in 2024 with a commanding 40.2% share, while BYD dominated PHEVs at 32%. By the end of 2026, Morocco’s total passenger EV fleet is estimated to hit 18,207 units. However, commercial EVs remain rare, with fewer than 100 units in operation.

Government Policies

The Moroccan government is actively supporting the EV market through financial incentives and policy initiatives. Corporations can enjoy purchase bonuses of up to MAD 100,000 (around $10,000), while all EVs benefit from full VAT exemptions and an 80% reduction in customs duties. Additionally, a government mandate requires that 30% of the state vehicle fleet must be electric or hybrid.

Morocco is also making strides as a manufacturing hub. The government has set an ambitious goal for 60% of automotive exports to be electric by 2030 and aims to achieve 80% renewable energy usage by 2050. Tesla entered the scene in June 2025 by establishing a local subsidiary and announcing a $2.8 million investment in an assembly plant in Kenitra, with plans to produce up to 400,000 vehicles annually. Meanwhile, Moroccan automaker Neo Motors launched full production of the "Dial-E" in January 2026, the country’s first fully designed and assembled EV, following its October 2025 debut.

Infrastructure Development

Morocco’s EV charging infrastructure is growing rapidly, though it remains concentrated in major cities like Casablanca, Rabat, and Marrakech. As of early 2025, the country had around 300 public charging points serving 2,500 EVs – an 8:1 ratio that surpasses the global benchmark of 10:1. Private companies have pledged $140 million to expand the network to 5,000 charging stations by 2028, aiming to support a projected fleet of 25,000 EVs by 2030.

In January 2026, FASTVOLT launched the first 360 kW ultra-fast charging station in Morocco. This facility, equipped with modular architecture, can charge up to six vehicles at once and features a 60 kWp solar canopy. It provides 62 miles of range in just about 5 minutes for high-voltage vehicles. FASTVOLT‘s network now includes over 200 connectors across 65 stations nationwide. These advancements are paving the way for further growth in Morocco’s EV sector.

Market Opportunities

Morocco is tapping into its natural resources to strengthen its EV ecosystem. The country’s phosphate reserves are a key driver for battery manufacturing investments. Gotion High Tech has pledged $1.3 billion for two gigafactories, while BTR New Material Group is investing $300 million in a cathode plant to produce lithium-iron-phosphate (LFP) batteries. A combination of local supply chain development and affordable imports from China is lowering barriers to entry and accelerating the growth of Morocco’s EV market.

Let’s Talk Electric Episode 5: Powering the future – SA’s 2026 NEV guide

3. Ghana

Ghana is carving its own path in the electric vehicle (EV) space, taking deliberate steps to shape its EV future.

EV Adoption Rates

Ghana’s journey with EVs is still in its early stages, with the National Electric Vehicle Policy (2024–2026) currently in development. By 2023, the country had approximately 17,000 plug-in EVs on the road. Between 2017 and 2021, Ghana imported 17,660 plug-in vehicles, with 53% being two- and three-wheelers and nearly all (98%) being battery electric vehicles.

While EVs are proving to be practical for daily commutes in the Greater Accra Region, longer intercity trips remain difficult due to the limited availability of highway charging stations. The government has set ambitious goals: achieving 35% EV penetration by 2035 and phasing out the sale and import of new gasoline and diesel vehicles by 2045. These targets highlight the need for strong policies to drive progress.

Government Policies

In December 2023, during COP28 in Dubai, Ghana unveiled its National Electric Vehicle Policy, signaling a firm commitment to transitioning to cleaner transportation. To make EVs more competitive, the government reduced import duties. Additionally, the Energy Commission is working on finalizing regulations for EV charging infrastructure and battery swap systems, with plans to oversee everything from manufacturing and imports to installation and operation.

"The passage of the draft regulations would empower the Energy Commission to effectively regulate and license all aspects of the EV infrastructure value chain, including the manufacturing, assembly, importation, installation, and operation of charging equipment and battery swap systems."

– Professor John Gartchie Gatsi, Board Chairman, Energy Commission

Efforts to stimulate local industry include electric bus assembly pilots and fiscal incentives for businesses. Ghana’s long-term vision involves a complete phase-out of internal combustion engine vehicles by 2070.

Infrastructure Development

Charging infrastructure remains a significant challenge in Ghana. By August 2024, the country had only seven public charging stations, making intercity travel difficult. To address this, the Ministry of Energy has pledged to install at least 100 rapid charging stations by 2029.

Private companies are also stepping up, placing chargers in convenient locations like workplaces and shopping malls. With over 80% of households having electricity access, many EV owners rely on home charging. A UNDP pilot project highlighted the benefits of EVs, showing that a single vehicle could save over $2,138 annually and reduce CO₂ emissions by 5.23 tons per year. The government is also prioritizing solar-grid hybrid charging stations along highways to enable longer trips. Expanding the charging network will be crucial for broader adoption.

Market Opportunities

Ghana is focused on building a domestic EV supply chain. Local companies like Kantanka and startups such as Mana Mobility are exploring opportunities in assembly and component manufacturing. However, high costs remain a barrier for consumers – for instance, the Hyundai Kona EV is priced at over $55,000.

The commercial sector is leading the way, with electric two-wheelers and ride-hailing fleets like Moove gaining popularity. As regulations solidify and infrastructure grows beyond Accra, the market is expected to expand, creating opportunities for manufacturers and service providers. Addressing the twin challenges of affordability and infrastructure will be key to sustaining momentum in Ghana’s EV sector.

4. Ethiopia

Ethiopia is making bold strides toward electrifying its transportation sector, becoming the first country to prohibit the import of gasoline and diesel-powered passenger vehicles starting in 2024.

EV Adoption Rates

This landmark ban has spurred a remarkable shift in the country’s vehicle market. Electric vehicle (EV) adoption surged from less than 1% of vehicles on the road to 6% in just two years (2024–2026). The total number of EVs in Ethiopia skyrocketed, growing from 4,600 in early 2023 to roughly 14,000 by early 2025. By February 2026, the number surpassed 100,000 EVs. The government has set ambitious goals to reach 148,000 EVs by 2030 and 500,000 by 2032. While Ethiopia’s overall vehicle fleet remains modest – 1.7 million vehicles for a population of 130 million – the pace of EV adoption is among the fastest in Africa.

Government Policies

Economic challenges have been a key driver for Ethiopia’s push toward EVs. The country spends over $4 billion annually on fossil fuel imports, a significant drain on its foreign currency reserves. After defaulting on sovereign bonds in 2023, the government ramped up its EV initiatives to conserve foreign currency and reduce reliance on imported fuel.

"Ethiopia’s EV policy reflects energy security as much as climate strategy. As a fuel importer with limited foreign exchange, replacing gasoline demand with locally generated electricity reduces exposure to oil price swings."

– Daba Finance

To encourage EV adoption, the government introduced a tiered tariff system that incentivizes local assembly. Fully assembled EVs are subject to a 15% duty, while semi-assembled units face a 5% duty, and fully knocked-down kits assembled locally are exempt from import duties. EVs are also exempt from VAT, excise taxes, and surtaxes. These policies have attracted investment, with 17 EV assembly plants operating as of February 2026 and plans to increase that number to 60 by 2030. Chinese manufacturers, such as BYD and Chang’an, dominate the market. For instance, the BYD Seagull, priced at approximately 3.6 million birr, is more affordable than many used gasoline sedans, which cost over 4.2 million birr.

Infrastructure Development

Ethiopia is complementing its policy measures with significant infrastructure projects. The Grand Ethiopian Renaissance Dam (GERD), which began operation in September 2025, generates 5,150 megawatts, effectively doubling the nation’s peak grid power. This clean energy source provides electricity at a rate of about $0.10 per kWh, supporting large-scale EV adoption. However, charging infrastructure is still concentrated in urban areas. As of February 2026, there were around 500 public charging stations, most of which are located in Addis Ababa. To address this, the government plans to install charging stations every 31 to 75 miles along major routes.

"The plan aims to make it less daunting for electric vehicle users to drive long distances without running out of power."

– Bahru Oljra, Executive Director of Energy Sector Control at the Petroleum and Energy Authority of Ethiopia

Despite the country’s robust electricity generation, only 55% of the population currently has access to electricity.

Market Opportunities

Ethiopia’s policy framework and growing infrastructure are creating new opportunities in the EV market. Chinese manufacturers like BYD and Chang’an dominate sales, while the 0% import duty on fully knocked-down kits has encouraged local assembly, opening doors for manufacturers and suppliers. Additionally, new restrictions on gasoline motorcycles have accelerated the adoption of electric alternatives, particularly for public procurement and delivery services.

While Ethiopia’s combination of fiscal incentives, renewable energy capacity, and proactive policies positions it as a leader in EV adoption, challenges remain. Limited access to credit and rising electricity tariffs could impact affordability and slow the pace of growth.

5. Nigeria

Nigeria is stepping up as West Africa’s leader in electric mobility, leveraging its large population and economic strength to advance sustainable transportation. By late 2025, there were between 15,000 and 20,000 electric vehicles on Nigerian roads, constituting just 0.5%–1% of the total vehicle fleet. While these numbers might seem small, the growth is undeniable – electric vehicle (EV) sales accounted for 7.11% of total car sales in 2022, up from 4.22% in 2020. Projections suggest the market will expand at a compound annual growth rate of 30.6% from 2025 to 2031.

EV Adoption Rates

The removal of fuel subsidies has significantly boosted EV adoption. With petrol prices ranging from ₦770 to ₦1,030 per liter, electric vehicles are becoming a more economical choice. This policy change also saves the government $3.7 billion annually. Urban hubs like Lagos and Abuja are leading the charge, with commercial applications – such as ride-hailing, last-mile delivery, and motorcycle-taxi services – driving demand. Electric motorcycles and scooters are particularly popular due to their affordability and practicality. These trends are paving the way for more government initiatives to accelerate adoption.

Government Policies

Nigeria is reinforcing its EV growth with supportive policies aimed at fostering local manufacturing and infrastructure development. The Electric Vehicle Transition and Green Mobility Bill, which passed its second reading in November 2025, requires foreign automakers to establish local assembly plants within three years and mandates that 30% of vehicle components be sourced locally by 2030. The government has set ambitious goals: achieve a 60% EV market share by 2050 and 100% by 2060. Under the National Automotive Industry Development Plan (NAIDP 2023), manufacturers benefit from zero import duty on EV components and a 10-year tax holiday. The 2025 bill also mandates the installation of EV charging points at all existing fuel stations.

"What the government is trying to do is to empower our local businesses and, most importantly, to reduce the price of electric vehicles. If 30% of whatever you need to assemble a car is sourced locally, it will have an impact on the price of the car."

– Ayodeji Audu, Founder and CEO of Reown

Infrastructure Development

Infrastructure remains a major hurdle, as Nigeria’s national power grid struggles with limited access and reliability. To address these challenges, the government plans to deploy 3,000 charging stations annually starting after 2030. Renewable energy solutions, such as solar-powered charging stations, are gaining traction, particularly in off-grid areas. Battery-swapping systems for two- and three-wheelers are also being introduced to reduce wait times and bypass grid limitations. Currently, only 55% of Nigeria’s population has access to electricity, making renewable energy integration a critical component for the EV ecosystem’s success.

Market Opportunities

Nigeria’s growing commercial sector and supportive policies are creating fertile ground for the EV market. Key players include Innoson Vehicle Manufacturing (the country’s first indigenous EV models), JET Motor Company (specializing in electric vans and buses), and MAX.ng (focused on electric motorcycle fleets). Domestic EV prices range from ₦12 million to ₦150 million ($7,800–$97,500), making affordability a significant challenge for the average consumer.

"The average user cannot afford to buy a used car outright. The demand for financing surged heavily, and for mass adoption to happen, the government needs to look into financing initiatives."

– Femi Oriowo, Co-founder and CEO of Carbin Africa

With a population expected to reach 375 million by 2050, Nigeria has the largest potential EV market in Africa. The combination of robust policies, local manufacturing incentives, and a thriving commercial sector positions the country as a pivotal player in Africa’s electric vehicle transformation – provided infrastructure issues are effectively addressed.

6. Kenya

Kenya is quickly establishing itself as a leader in East Africa’s electric vehicle (EV) market, with registrations skyrocketing by an incredible 2,700% – from just 1,378 EVs in 2022 to a projected 39,324 by 2025. This growth places Kenya well ahead of its regional neighbors, including Uganda (3,200), Tanzania (1,850), and Rwanda (1,200). In February 2026, the Kenyan government formally introduced its National Electric Mobility Policy, designed to cut down on the country’s $5 billion annual petroleum import bill while promoting cleaner transportation options. These developments highlight Kenya’s rapid progress in EV adoption.

EV Adoption Rates

Electric two-wheelers, commonly referred to as boda bodas, dominate Kenya’s EV market, with over 35,000 registered by 2025. Corporate fleets make up about 68% of all registered EVs, with major companies like Safaricom leading the way. Safaricom, for example, operates 120 electric vehicles and plans to electrify 30% of its 2,000-vehicle fleet. The cost advantage is clear: charging an EV costs about 60% less than fueling a gas-powered vehicle, with electricity for charging priced at an average of $0.35 per kWh – much cheaper than gasoline. Starting in January 2025, the government mandated that all new public service vehicles be electric, impacting approximately 3,000 vehicles annually. By 2025, electricity consumption for EV charging more than doubled to 8.4 million kWh, generating $976,803 in revenue for Kenya Power.

Government Policies

Kenya’s government has implemented aggressive policies to encourage EV adoption. VAT has been removed for electric buses, bicycles, motorcycles, and lithium-ion batteries, while excise duty on e-bikes and motorcycles has been completely eliminated. EV assemblers also benefit from reduced excise duty (10%) and are exempt from the standard 35% import duty on assembly kits. Additionally, a special electricity tariff for EVs offers off-peak rates of $0.06 per unit and $0.12 during peak hours, encouraging nighttime charging to ease grid demand. To further support EV infrastructure, all new commercial buildings must allocate at least 5% of parking spaces for EV charging, and green license plates now distinguish fully electric vehicles. Scheduled for July 2026, additional tax breaks for EV parts and charging equipment will further boost the market.

"Over 90% of the electricity we supply comes from renewable sources, ensuring that electric mobility is not only innovative but also sustainable." – Joseph Siror, Managing Director, Kenya Power

Infrastructure Development

While adoption rates are impressive, infrastructure development still has room to grow. Charging stations are mostly concentrated in Nairobi and nearby areas, with dozens of stations for cars and hundreds of battery-swap points for two-wheelers. However, charger installation has struggled to keep up with vehicle deliveries, leaving some transport operators with less than half their electric buses operational within a year. Another challenge is the lack of interoperability between charging platforms, which forces reliance on isolated private networks and creates technical fragmentation. Battery swapping has proven to be a more flexible solution than fixed charging, which explains the popularity of electric motorcycles and bicycles. The government aims to address these gaps by deploying 10,000 public charging stations by 2030, but delays in utility upgrades and lengthy approval processes remain obstacles.

Market Opportunities

Kenya’s favorable policies and rising demand are fueling local manufacturing efforts. TAD Motors, for example, plans to produce 3,000 compact EVs annually near Nairobi, priced at about $10,000 each to compete with used imports. In February 2026, Rideence Africa partnered with Associated Vehicle Assemblers in a $2.46 million deal to open Kenya’s first dedicated EV assembly line in Mombasa. Meanwhile, Roam Electric has sold 85 electric buses to public transport operators, with each bus saving an estimated $62,000 in annual operating costs compared to diesel alternatives. The International Finance Corporation has also taken notice, announcing a $5 million equity stake in ARC Ride to support its automated battery-swap network. With over 90% of Kenya’s electricity coming from renewable sources, the country is well-positioned to sustain its EV ecosystem – provided infrastructure can keep up with the growing demand.

7. Rwanda

Rwanda’s move toward electric mobility has been nothing short of dramatic, with the number of EVs jumping from just 19 in 2020 to over 7,000 EVs and hybrids projected by 2026. A major catalyst for this shift is the government’s decision to ban new petrol motorcycle registrations in Kigali starting in 2025. This policy is especially impactful since motorcycle taxis make up over 80% of the country’s motorcycles.

Government Policies

Rwanda has introduced a range of incentives to accelerate EV adoption. EVs and hybrids are exempt from import duties and VAT, cutting their tax burden by 48%. Investors in the e-mobility sector benefit from a reduced 15% corporate tax rate, seven-year tax holidays, and access to rent-free land. To support charging station development, building codes have been updated. EV owners also enjoy perks like green license plates, free parking, and access to congestion zones. Additionally, electricity for charging EVs is subsidized at $0.10 per kWh, half the standard rate of $0.20 per kWh. By 2030, the government aims to electrify 20% of buses, 30% of motorcycles, and 8% of cars.

Infrastructure Development

Kigali is leading the way in charging infrastructure with 200 charging stations – 35 dedicated to electric cars and 165 for motorbikes. In 2024, the Rwanda Green Fund partnered with e-mobility company Kabisa through its Ireme Invest initiative to expand this network, adding 35 car-specific charging stations as part of a $900 million strategic investment. However, these advancements are primarily concentrated in Kigali, leaving rural areas and long-distance travelers with limited charging options.

Market Opportunities

For Rwanda’s 46,000 registered motor-taxi riders, the switch to electric motorcycles presents clear economic advantages. A single battery charge covering 60 km (37 miles) costs between $1.00 and $1.50, compared to $1.30 per liter of petrol, which only covers 35 km (22 miles). This translates to daily savings of around $2 per rider. Companies like Spiro are making electric motorcycles more accessible, offering models at just $500. The shift to electric motorcycles is expected to save Rwanda $6.6 million annually in fuel import costs. Over five years, the total cost of owning an electric vehicle is estimated at $41,000, compared to $44,160 for a petrol vehicle. Maintenance costs also drop significantly, from $1,200 annually for petrol vehicles to $400 for EVs.

These combined efforts highlight Rwanda’s dedication to creating a well-rounded and forward-thinking EV ecosystem.

Advantages and Challenges

Examining the diverse strategies across Africa’s EV markets reveals both opportunities and hurdles. Ethiopia’s bold decision to ban non-electric vehicle imports has driven EV registrations to dominate, now making up over 60% of new vehicle sales. Morocco has emerged as a manufacturing leader, with multi-billion-dollar investments in battery production and ambitious production goals. South Africa, on the other hand, boasts a well-developed charging network with over 316 stations, though the reliability of home charging is often undermined by frequent power outages.

Infrastructure development shows significant disparity across the continent. For instance, while BYD is planning to install 200–300 public chargers in South Africa by 2026, Ghana currently operates only seven public charging stations despite having approximately 17,000 EVs on its roads by the end of 2023. Rwanda has taken a unique approach by banning new petrol motorcycle registrations in Kigali and expanding its battery swap networks. Meanwhile, Nigeria and Kenya are adopting forward-looking solutions, with companies like Spiro deploying over 60,000 electric motorbikes and establishing 1,500 battery swap stations in these markets by October 2025.

The potential of each market is tied to factors like affordability and local production capabilities. Ghana, for example, has leveraged an eight-year zero-tariff policy on EV imports to secure roughly 29% of Africa’s EV market by 2025. Meanwhile, South Africa attracts Chinese brands with stable financing options and vehicle prices ranging from $19,865 to $46,847. Ethiopia’s market is set to grow at a staggering 56.9% compound annual growth rate through 2031, thanks to its strong policy initiatives and reliance on a predominantly hydro-powered grid.

"Even the world’s leading EV markets fall short of Ethiopia’s aggressively pro-EV policies. In 2024, the country became the first in the world to ban the import of non-electric private vehicles."

- MIT Technology Review

One striking trend across the continent is the dominance of two-wheelers over passenger cars. By 2025, electric motorbikes accounted for 45% of new vehicle sales globally, compared to just 25% for cars and trucks. This pattern is especially evident in countries like Rwanda, Kenya, and Nigeria, where battery swap systems help offset high upfront costs and address grid reliability issues. As Nelson Nsitem, Lead Africa Energy Transition Analyst at BloombergNEF, notes:

"There’s already some local assembly of electric two-wheelers in countries including Morocco, Kenya, and Rwanda."

These developments highlight both the progress and challenges shaping Africa’s transition to electric mobility, setting the stage for broader discussions on the continent’s future in this space.

Conclusion

The electric vehicle (EV) landscape across Africa in 2026 showcases a mix of opportunities and challenges. Ethiopia’s ban on non-electric private vehicle imports, backed by affordable hydropower, and Morocco’s $5.6 billion battery gigafactory highlight how strong policies and infrastructure investments can accelerate EV adoption. These examples demonstrate that government initiatives play a key role in shaping the future of EVs in the region.

On the other hand, countries like Nigeria face significant obstacles. Limited infrastructure, unreliable power supply, and an oil-dependent economy present major barriers. Nigeria’s transportation sector alone accounts for 48% of its annual CO₂ emissions, and the lack of charging stations combined with a fragile grid complicates efforts to integrate EVs. As ScienceDirect notes:

"The reluctance in Nigeria can be rationalized by its economic structure, which is heavily reliant on oil revenue, acting as a substantial obstacle to quick EV acceptance".

These regional differences underline the need for tailored approaches. For instance, electric two- and three-wheelers accounted for around 45% of new vehicle sales in 2025, compared to just 25% for cars and trucks, reflecting the demand for affordable and practical mobility options. Battery swapping models, like Spiro’s rollout of 60,000 electric motorbikes and 1,500 swap stations, further illustrate the region’s focus on cost-effective solutions. Kelly Carlin from the Rocky Mountain Institute highlights the transformative potential of economies of scale:

"You have very high-quality, very affordable vehicles coming onto the market that are benefiting from the economies of scale in China. These countries stand to benefit from that. It’s a game changer".

To capitalize on these developments, businesses and investors should consider strategic partnerships with established manufacturers like BYD, which plans to expand to 70 dealerships in South Africa by 2026. Local assembly operations in countries such as Morocco, Kenya, and Rwanda can help reduce import costs, while pairing solar-powered charging stations with existing infrastructure can address grid limitations. Additionally, creating standardized, cross-border charging systems could support broader regional growth.

Africa’s EV potential is as diverse as its nations. Success depends on aligning strategies with local realities, leveraging government incentives, and focusing on practical solutions like electric motorcycles and battery-swapping networks. By addressing these unique challenges, the region can pave the way for a more sustainable and accessible mobility future.

FAQs

Which African country is best for buying an EV in 2026?

South Africa has positioned itself as the leading destination in Africa for electric vehicle (EV) ownership in 2026. With over 450 charging stations already in place, the country boasts the most developed EV infrastructure on the continent. This network ensures that drivers have access to convenient charging options, a critical factor for EV adoption.

The government has also stepped up with strong incentives to encourage EV production and ownership. A standout policy is the 150% tax deduction for companies involved in EV manufacturing, which has spurred growth in the sector. On the consumer side, the market reflects this momentum, with 6,000 EVs already on the road.

Of course, South Africa isn’t without its challenges. The country’s power grid has faced well-documented issues, which could pose hurdles for widespread EV adoption. However, its advanced infrastructure and supportive policies still give it a clear edge over other African nations like Kenya and Morocco, where EV markets are still in earlier stages of development.

For anyone considering an EV in Africa, South Africa’s combination of infrastructure, incentives, and market growth makes it the top choice.

Can I road-trip between cities with today’s charging networks?

Road-tripping between cities in Africa can be done in areas like Southern, Northern, and parts of East Africa, where the charging infrastructure is relatively more established. That said, the availability of charging stations still varies greatly across the continent. While there are hundreds of public chargers, including some solar-powered options, it’s essential to plan your route carefully to ensure you’ll have access to charging points when needed.

Are electric motorcycles a better deal than electric cars in Africa?

Electric motorcycles are becoming a smart choice in Africa, thanks to their affordability, ease of use, and versatility across both urban and rural settings. Perfect for short commutes and small-scale commercial activities, these bikes offer a practical solution for many. On the other hand, electric cars face hurdles like a lack of widespread charging infrastructure. While the overall cost of owning an electric car is predicted to get better in the future, motorcycles remain the more accessible and cost-effective option for most individuals and businesses today.